Rate rises over: OECD says inflation pressures now under control

The Reserve Bank does not need to inflict any more pain on home buyers and will probably have to start cutting interest rates next year, says the Organisation for Economic Co-operation and Development in a new report released as evidence grows that inflation pressures are starting to ease.

In its global economic outlook released on Wednesday night, the Paris-based think tank revealed it believes the official cash rate has peaked at its current level of 4.35 per cent and expects the RBA to cut rates by three-quarters of a percentage point through the second half of 2024 and into early 2025.

Forecasting economic growth to slow from 1.9 per cent to 1.4 per cent next year, and for the unemployment rate to edge up to 4.4 per cent in mid-2025, the OECD said higher official interest rates around the globe were bringing inflation back under control.

It argued previous rate increases, on top of overall cost pressures on Australians, meant it was unlikely the Reserve Bank would have to proceed with further interest rate hikes to get inflation back inside its target band.

“The accumulated impact of higher interest rates and cost-of-living pressures will damp spending by households and businesses over the coming year, though this will be partly offset by continued strong working-age population growth and the ongoing recovery in education and tourism exports,” it said.

Reserve Bank governor Michele Bullock has made clear the institution is prepared to lift official interest rates even further to bring inflation down, telling a conference in Hong Kong this week that despite many people being “very unhappy” with the RBA’s recent decisions they were dealing well with higher mortgage repayments.

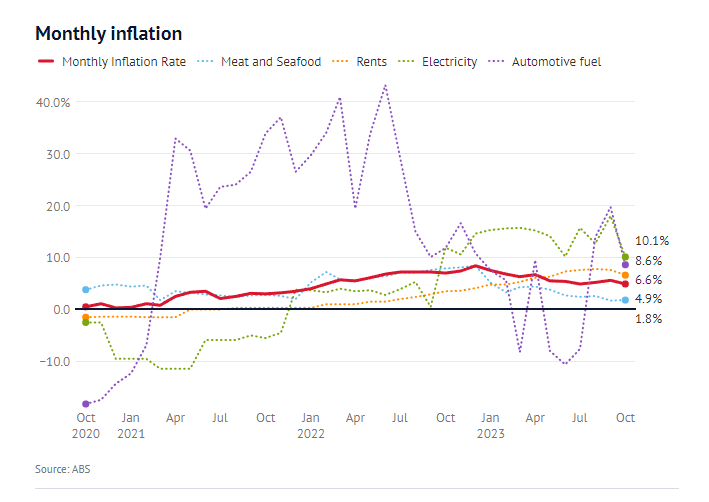

Figures from the Australian Bureau of Statistics suggest the Reserve Bank’s sharp increase in interest rates is working, with the monthly measure of inflation falling to 4.9 per cent in October. It had been 5.6 per cent in September.

Financial markets had been expecting inflation to slow to 5.2 per cent.

In monthly terms, prices fell by 0.4 per cent – the biggest one-month drop since September 2020.

Taking out volatile items such as petrol, holiday travel, fruit and vegetables, underlying inflation also fell sharply in the month, dropping to 5.1 per cent. It had been at 5.5 per cent in September.

One of the biggest factors in inflation, rents, fell from an annual rate of 7.6 per cent to 6.6 per cent as the federal government’s changes to Commonwealth rent assistance started filtering through the property market. In monthly terms, rent prices fell by 0.4 per cent.

Costs for building a new home peaked at almost 22 per cent in the middle of last year due to strong demand and international supply chain problems. That has now fallen to a 26-month low of 4.7 per cent.

The annual rate of inflation for food and non-alcoholic drinks increased to 5.3 per cent from 4.7 per cent, but in the month, prices were up by just 0.1 per cent. Fruit and vegetable prices were up, in part due to a reduced supply of melons and bananas.

People were feeling the strain of having paid more for goods at a market in Melbourne’s south on Wednesday, where shoppers acknowledged recent inflationary pressure had meant accepting they’d be paying more for fresh produce.

Remy Muller said he was buying fewer quality cuts of meat for his family of four. At $5 a punnet, he said the blueberries had been left on the shelf during this week’s shop too.“It’s everywhere the same now, unfortunately, we have to ride the wave,” he said.

Petrol prices are also starting to ease. The annual rate of inflation of automotive fuel was 19.7 per cent in September but this eased to 8.6 per cent in October.

Through October, prices fell by 2.9 per cent after jumping by 3.3 per cent in September.

The monthly measure of inflation, which peaked at 8.4 per cent late last year, could be under 4 per cent by the end of the year and lower than wages growth for the first time in almost two years.

The better-than-expected figures had an immediate impact, with the ASX200 jumping in value as investors bet interest rates will not have to be pushed higher.

Financial markets, which had put the chances of a rate rise next year at 60 per cent, pared that to no better than 50-50.

Betashares chief economist David Bassanese said the inflation figures, on top of this week’s retail trade report which showed a 0.2 per cent fall in sales during October, would deliver the Reserve Bank comfort that current interest rate settings were working.

“In the space of two days, therefore, we’ve received reassuring news that both consumer spending and inflation continue to ease, which should obviate the need for the RBA to dampen Christmas cheer with another rate increase next week,” he said.

ACTU secretary Sally McManus said the figures were confirmation the Reserve Bank should not add to financial pressures on ordinary people who were being hit by businesses seeking to protect their profit margins.

“The RBA should stop worsening the financial stress of working people when the evidence is clear that corporate profiteering and price gouging is compounding inflation. Every time they put up interest rates, landlords pass the pain on through higher rents,” she said.

But some analysts are yet to be convinced. Deutsche Bank Australia senior economist Phil O’Donoghue said if the Reserve Bank does not lift interest rates at its board meeting on Tuesday it would hit home buyers early next year.

“Any delay beyond December only increases the chance that RBA needs to hike more than once in the new year, and with that would come a delay to the timing of any cuts,” he said.